Present Day Use Case Scenarios of Data Labeling in Insurance Sector

AI’s application in the insurance industry is expanding rapidly, covering everything from risk mitigation and damage analysis to compliance and claims processing. For example, repetitive activities are performed by Robotic Process Automation (RPA), freeing up operational personnel to work on more complicated duties.

AI is radically altering the long-standing practices of insurance. The sector is predicted to surpass $2.5 billion by 2025 because of its quick growth. This benchmark suggests a 30.3% compound annual growth rate from 2019 to 2025.

Use Cases of AI ML & Data Labeling in Insurance Sector

Fraud Detection in Insurance Claims:

Research conducted by the FBI on US insurance firms found that the annual cost of insurance fraud, or non-health insurance, is around $40 billion. This indicates that the average US household pays an additional $400 to $700 a year in premiums as a result of insurance fraud. These alarming figures highlight how urgently insurance firms need extremely accurate automated theft detection systems to improve their due diligence procedures.

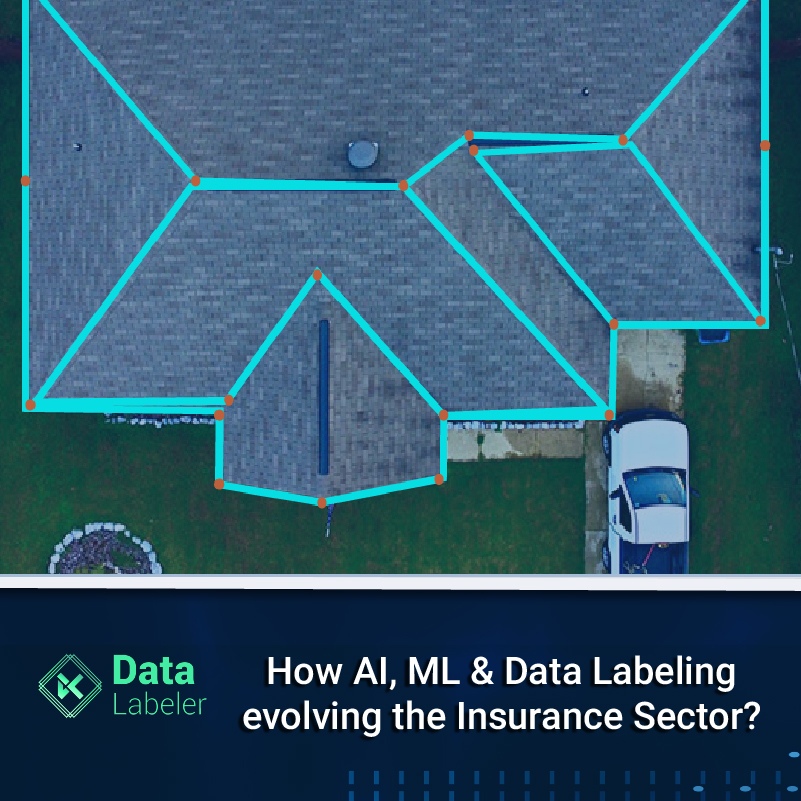

Analysis of Property Damage:

Insurance companies face a difficult problem when calculating repair costs through manual intervention in damage assessment. According to a PwC analysis, using drones and artificial intelligence in the insurance sector can save the sector up to US$6.8 billion annually. By combining automated object detection with the power of drones, claim resolution times can be shortened by 25% to 50%. Vehicle parts deterioration can be identified using machine learning models, which can also assist in estimating repair costs.

Automated Inspections:

The procedure of filing a damage insurance claim begins with an inspection, regardless of the asset—a mobile phone, a car, or real estate. Manual inspection is an expensive proposition because it necessitates the adjuster/surveyor to travel and engage with the policyholder. Inspections can cost anything from $50 to $200. Since creating and estimating reports takes one to seven days, claims settlement would also be delayed.

Insurance firms can examine car damage with AI-powered image processing. After that, the system produces a comprehensive assessment report that lists all vehicle parts that can be repaired or replaced along with an estimate of their cost. Insurance companies can reduce the cost of estimating claims and streamline the procedure. In addition, it generates reliable data to determine the ultimate settlement sum.

Automated Underwriting :

Traditionally, the analysis of past data and decision-making in insurance underwriting relied mostly on employees. In addition, they had to deal with disorganized systems, processes, and workflows to reduce risks and give value to customers. Intelligent process automation offers Machine Learning algorithms that gather and interpret vast volumes of data, streamlining the underwriting process.

Moreover, it minimizes application mistakes, controls straight-through-acceptance (STA) rates, and enhances rule performance. Underwriters can concentrate solely on challenging instances that may necessitate manual attention by automating the majority of the procedure.

Pricing and Risk Management:

Price optimization uses data analytic techniques to determine the optimal rates for a particular organization while taking its goals into account. It also helps to understand how customers respond to various pricing strategies for goods and services. Generalized Linear Models, or GLMs, are primarily used by insurance companies to optimize prices in areas such as life and auto insurance. By using this strategy, insurance businesses can improve conversion rates, balance capacity, and demand, and gain a deeper understanding of their clientele.

Automation of risk assessment also improves operational effectiveness. Automation of risk assessment increases efficiency by fusing RPA with machine learning and cognitive technologies to build intelligent operations. Insurance companies can provide a better customer experience and lower turnover because the automated procedure saves a lot of time.

Here’s how Fraud Detection can be achieved from Data Labeling?

Fraud detection systems that use machine learning (ML) rely on algorithms that can be taught with historical data from both legitimate and fraudulent acts in the past. This allows the algorithms to autonomously discover patterns in the events and alert users when they recur.

Large volumes of labeled data, previously annotated with specific labels characterizing its main attributes, are used to train ML-based fraud detection algorithms. Data from both genuine and fraudulent transactions that have been labeled as “fraud” or “non-fraud” accordingly may be included in this. The system receives both the input (transaction data) and the desired output (groups of classified examples) from these labeled datasets, which is significantly a laborious manual tagging process. This allows algorithms to determine which patterns and relationships link the datasets and use the results to classify future cases.

In addition to the areas highlighted above, there are a few more in the insurance industry

where AI & Data Labeling are essential to delivering the best possible client experience.

- Customer segmentation

- Workstream balancing for agents

- Self-servicing for policy management

- Claims adjudication

- Policy Servicing

- Insurance distribution

- Speech analytics

- Submission intake and many more

If you want to create a faster and better experience for your customers in the Insurance

field, please visit our website Data Labeler, and contact us.

admin

admin

November 08, 2023

November 08, 2023